Types of Trusts

An irrevocable asset protection trust when combined with a Limited Liability Company is an asset protection fortress, short of a foreign asset protection trust. A foreign asset protection trust is the Rolls Royce of asset protection, the irrevocable trust with an LLC is the Cadillac.

If you own titled assets and want your loved ones (spouse, children or parents) to avoid court interference at your death or incapacity, you should probably have a living trust. You may also want to encourage other family members to have one so you won't have to deal with the courts at their incapacity or death.

A safe-deposit box at a local bank or credit union may be the best place to store hard-to-replace documents, jewelry and other small valuables. But it could be the worst place for certain other items. Here’s a quick run-down of what to keep in — and keep out of — your safe-deposit box. Leave these out. 1. The only copy of your will.

We can alleviate that with a well-planned & executed business succession plan. ... Intellectual Property; ... Trusts & Estates | Business Interests.

A charitable trust described in Internal Revenue Code section 4947(a)(1) is a trust that is not tax exempt, all of the unexpired interests of which are devoted to one or more charitable purposes, and for which a charitable contribution deduction was allowed under a specific section of the Internal Revenue Code.

A constructive trust is not a trust, in the true meaning of the word, in which the trustee is to have duties of administration enduring for a substantial period of time, but rather it is a passive, temporary arrangement, in which the trustee's sole duty is to transfer the title and possession to the beneficiary.

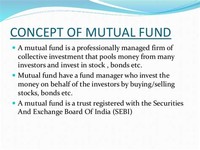

Unlike CDs, you can add or withdrawal funds to your MMA; however, there is a federal limit of six transactions per month, including writing checks or charging with a debit card. Interest is compounded and paid out either monthly or quarterly. Stocks, Bonds, Mutual Funds, and ETFs. Stocks, bonds, mutual funds and ETFs carry much more risk than CDs and MMAs. They do, however, offer much higher ...

Irrevocable trusts, such as irrevocable life insurance trusts, are commonly used to remove the value of property from a person’s estate so that the property can't be taxed when the person dies. In other words, the person who transfers assets into an irrevocable trust is giving over those assets to the trustee and beneficiaries of the trust so that the person no longer owns the assets.

The irrevocable life insurance trust or "ILIT" is a trust that cannot be rescinded, amended or modified in any way after its creation. Once the grantor contributes property or life insurance death benefits to the trust, he or she cannot change the terms of the trust or reclaim any property left to the trust.

Note, if you live in a community property state, the loan may be community property: in which your spouse or domestic partner owns an interest. Debts Owed May Reduce Heir's Inheritance To the extent an heir has failed to repay a loan made by the testator, the unpaid amount may be used to reduce any inheritance the heir would otherwise receive from the estate.

Real Estate Placed in a Living Trust If you are the sole owner of a piece of property, you can include that property in your living trust. You will need to change the property's title to reflect the ownership change.

With a revocable trust, however, you can place property into the trust and at some point in the future, undo the transfer by removing the property and terminating the trust. Very often, if you die or become incompetent, the provisions of a revocable trust call for the trust to become an irrevocable trust.

How a Special Needs Trust Can Help. A way around losing eligibility for SSI or Medicaid is to create what's called a special needs or supplemental needs trust. Then, instead of leaving property directly to your loved one, you leave it to the special needs trust.

A spendthrift trust is a trust that is created for the benefit of a person (often unable to control his spending) that gives an independent trustee full authority to make decisions as to how the trust funds may be spent for the benefit of the beneficiary.

Let's suppose your will sets up a bypass trust for your husband, and you die first. In order to keep the trust from being subject to estate tax when your husband dies, your will must place the following conditions on the trust: 1. You must limit your husband's power to access the trust during his lifetime.